The Reserve Bank of Zimbabwe (RBZ) unveiled its latest Monetary Policy Statement (MPS) last Friday in a climate of cautious optimism and deeply-contested economic realities.

Industry advocacy organisation Buy Zimbabwe welcomed the statement, hailing it as a positive step for local producers. But economic analysts have offered a more nuanced — and at times sharply critical — assessment.

The MPS touches on several fundamental issues — currency strategy, the dismantling of banking charges, inflation control and the thorniest issue of all — the continued maintenance of a 35% bank policy rate, the highest in Africa.

2030 mono-currency deadline

Among the most widely-discussed announcements is the RBZ's decision to move away from its previously stated 2030 timeline for adopting a mono-currency regime.

For years, businesses and investors operated under the assumption that Zimbabwe was marching toward a single currency economy anchored by Zimbabwe Gold (ZiG). The admission that this target is no longer fixed introduces both relief and anxiety.

On the one hand, it removes the pressure of an artificial deadline that many economists viewed as unrealistic. On the other, it reinforces the perception of continued monetary uncertainty.

- Open letter to President Mnangagwa

- Feature: ‘It’s worse right now than under Mugabe’: Sikhala pays the price of opposition in solitary cell

- Masvingo turns down fire tender deal

- Human-wildlife conflict drive African wild dogs to extinction

Keep Reading

Buy Zimbabwe has interpreted the move positively, arguing that abandoning the rigid deadline could help reduce policy uncertainty and support investor confidence in local industry.

However, the shift also reflects a familiar pattern in Zimbabwe’s economic management — stepping back from previously stated monetary commitments. Historically, such reversals have eroded public trust in policy frameworks.

Reduction, scrapping of bank charges

One of the more broadly welcomed provisions in the MPS is the scrapping and reduction of banking charges.

Banks will no longer be allowed to rely heavily on transactional charges, theoretically forcing them to pursue more productive revenue streams through lending.

Historically, Zimbabwean banks have generated significant income from transaction fees rather than credit intermediation. This has distorted the banking model and limited the flow of credit into the productive economy.

Removing this comfort zone should, in theory, push banks toward deeper lending activity.

However, whether this translates into meaningful and affordable credit will depend heavily on what happens to the interest rate environment.

Redesigned ZiG notes

The RBZ governor also announced the rollout of newly-redesigned ZiG bank notes.

While this may improve convenience in everyday transactions, the deeper challenge lies not in the design of the notes but in public confidence in the currency itself.

Only about 30% of Zimbabweans currently transact in ZiG, with the majority still relying on the US dollar.

This behaviour reflects Zimbabwe’s painful currency history — from the hyperinflation collapse of 2008 to the bond note and RTGS dollar episodes that followed.

Restoring confidence in the local currency will ultimately depend less on cosmetic redesigns and more on sustained macroeconomic credibility.

The 35% rate: A critical examination

The most contested element of Zimbabwe’s monetary policy framework — and conspicuously absent from Buy Zimbabwe’s otherwise warm endorsement — is the bank policy rate, which remains fixed at 35% per annum.

Since the RBZ raised the rate from 20% to 35% in September 2024, following a sharp devaluation that wiped out 43% of ZiG’s value, the rate has remained unchanged.

In regional context, Zimbabwe’s rate is extraordinary.

Most Southern African Development Community (Sadc) countries maintain policy rates averaging about 6,75%. Nigeria, grappling with its own inflationary pressures, currently sits around 27%. Botswana and South Africa maintain rates of roughly 7% to 7,5%.

Zimbabwe’s policy rate is therefore not merely elevated — it is the most aggressive monetary stance on the continent.

Governor John Mushayavanhu has defended the policy, arguing that it has helped drive a steady disinflation trajectory.

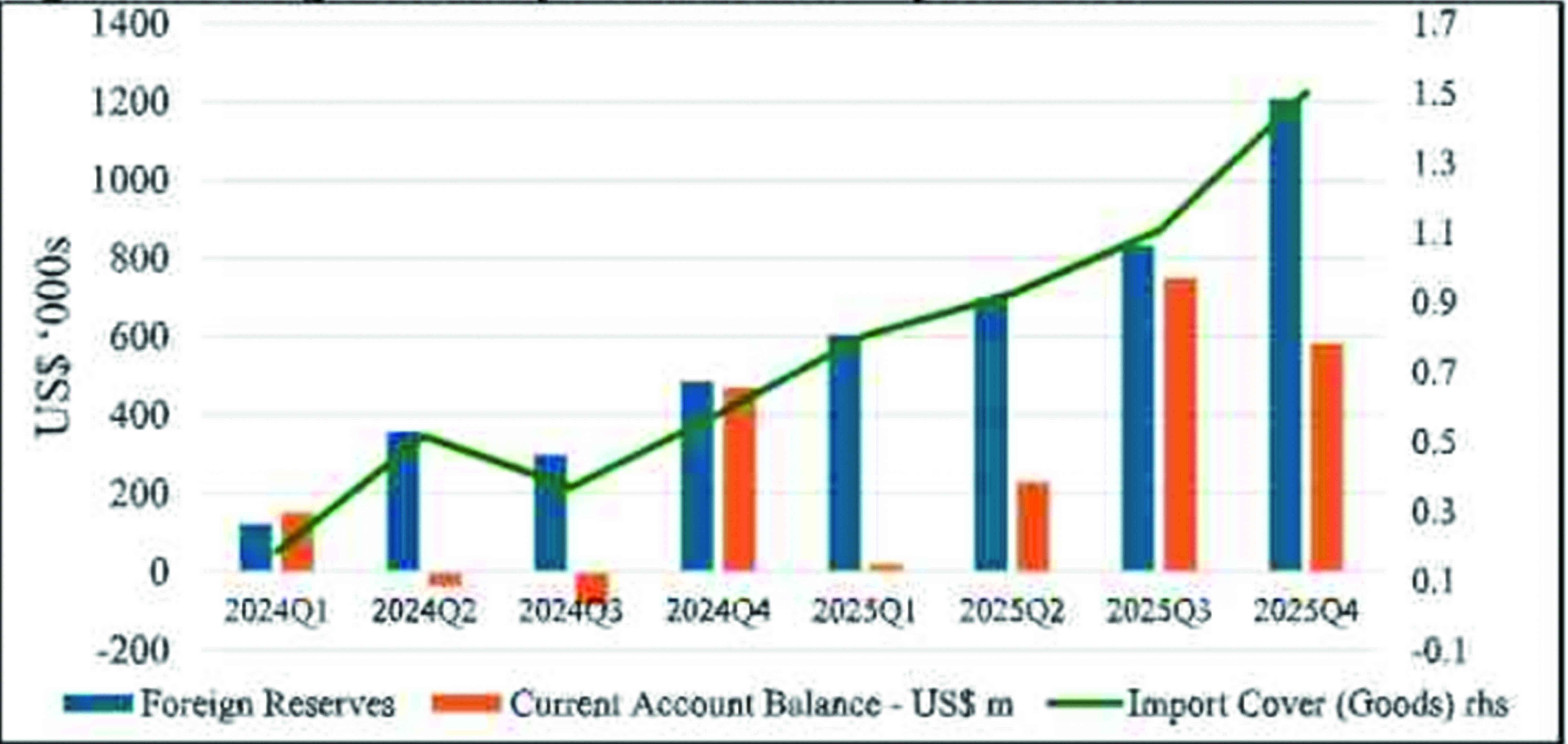

Monthly ZiG inflation has slowed dramatically, reaching 0,3% by mid-2025. The International Monetary Fund (IMF) has broadly supported the RBZ’s hawkish stance, noting that halting monetary financing and tightening reserve requirements were instrumental in stabilising the exchange rate.

Meanwhile, the World Bank has projected Zimbabwe’s GDP growth at about 6,6% for 2025, supported by a strong agricultural season, record gold prices and sustained remittance inflows estimated at US$2,45 billion.

The RBZ has warned that cutting rates prematurely could reverse these gains. The governor has argued that renewed inflationary pressures might force the central bank to tighten even further, creating higher economic and social costs.

This caution is understandable for a country that once experienced some of the worst hyperinflation in recorded history.

Yet the cost of this tight stance is increasingly visible across Zimbabwe’s productive sectors.

The real impact on economy

Cafca Limited, Zimbabwe’s only listed cable manufacturer and a company with more than 77 years of operating history, offers a stark illustration of what tight monetary policy means at factory level.

The company has warned that persistent foreign currency shortages and liquidity constraints pose risks to its continued operations.

The experiences of companies such as Wildale and other Zimbabwe Stock Exchange listed manufacturers mirror Cafca’s trajectory.

Across Zimbabwe’s formal productive sector, the 35% policy rate has cascaded into extremely high lending costs.

Commercial lending rates for ZiG-denominated loans have climbed above 45%, while US dollar facilities carry rates between 10% and 16% — still significantly higher than regional norms.

For capital-intensive industries that require long term financing for retooling, infrastructure investment and working capital, these rates represent a formidable barrier.

Art Holdings Limited — manufacturer of Exide batteries and Eversharp pens — reported that working capital constraints disrupted production volumes during the period ending December 2025.

Delta Corporation’s finance director similarly acknowledged that although the beverages giant maintains long-standing relationships with local banks, the prevailing interest rate regime and risk-averse lending criteria make it difficult to access the full range of financing needed to sustain growth.

The SME Association of Zimbabwe says many small businesses have largely retreated from the formal banking system altogether, relying instead on informal borrowing networks, savings cooperatives and microfinance institutions.

With limited access to credit outside banks and capital markets, many Zimbabwean firms have shifted into survival mode.

Internally generated funds have become the only viable source of investment capital.

This strategy has a name in economic terms — stagnation.

When companies cannot borrow to invest, they do not expand. When they do not expand, they do not hire. When employment stagnates, consumer demand remains suppressed — further weakening the very industries monetary policy is meant to support.

Structural contradictions in the MPS

The MPS also presents several internal tensions that merit closer scrutiny.

Inflation is falling sharply. The RBZ’s own projections suggest monthly ZiG inflation could stabilise below 1% this year, with annual inflation remaining in single digits.

If disinflation is already embedded, economists argue, the case for maintaining Africa’s highest policy rate becomes increasingly difficult to justify.

Standard IMF monetary policy sequencing suggests that once inflation expectations stabilise, central banks should begin a gradual easing cycle to avoid unnecessary output suppression.

Zimbabwe’s continued resistance to easing risks overcorrecting — controlling inflation at the expense of growth.

The scrapping of transaction charges also raises practical questions.

If banks are expected to replace this lost revenue with lending income, they must be able to lend at rates businesses can realistically service.

Lending above 45% to ZiG borrowers does not represent meaningful financial intermediation.

It represents a debt trap.

Similarly, redesigned banknotes address convenience rather than confidence. With only about 30% public uptake of ZiG despite its legal tender status since April 2024, the RBZ still faces a deep behavioural challenge rooted in decades of currency instability.

Exporters have also raised concerns over the foreign currency surrender requirements.

Manufacturers and tobacco farmers argue that mandatory surrender of export proceeds at the official RBZ exchange rate — while the parallel market trades at a premium — effectively taxes them at the point of revenue generation.

The Zimbabwe Farmers Union recently criticised the increase in the surrender threshold from 25% to 30%, warning that it erodes margins for exporters who must import machinery, spare parts and agricultural inputs using hard currency.

This tension between the RBZ’s liquidity management objectives and the operational realities of export industries remains unresolved.

What the MPS could have done differently

A more comprehensive policy package might have included a transparent roadmap for interest rate normalisation.

Instead of defending the 35% rate indefinitely, the RBZ could outline clear inflation thresholds that would trigger gradual rate reductions. Such guidance would provide businesses with planning certainty and signal that tight policy is a temporary stabilisation tool rather than a permanent feature of Zimbabwe’s monetary landscape.

The central bank could also expand targeted lending frameworks that offer subsidised financing to productive sectors such as agriculture, manufacturing and export industries.

The one way convertibility problem highlighted by companies like Cafca also requires urgent attention.

A currency that cannot be easily converted back into US dollars discourages adoption and reinforces the very dollarisation the RBZ seeks to reverse.

Finally, Zimbabwe’s domestic capital markets remain shallow.

The country has limited bond issuance activity, and the Zimbabwe Stock Exchange has struggled to facilitate significant capital raises.

Developing deeper and more regulated capital markets could reduce the economy’s reliance on expensive short term bank credit while providing manufacturers with longer term financing options.

The RBZ’s latest MPS

represents a genuine — if cautious — attempt to consolidate stability in an economy scarred by repeated monetary crises.

But the next chapter of Zimbabwe’s monetary story must balance hard-won inflation control with a renewed commitment to affordable capital for industry.

Stabilising Zimbabwe’s economy is an important first step.

Expanding it will require an honest national conversation about the price of money. — Equity Axis News.